First thing first, does highest NAV mean highest ROI? Nope, they say that it is the highest of whatever they can manage to attain. It is very unlikely that with such a guarantee in place, they can provide even bench mark returns.

Let’s have a close look at how a possible highest NAV plan will work. They use Dynamic Hedging and Constant Proportion Portfolio Insurance. Although I don't fully understand these concepts, we actually don't need to digest this financial alchemy. Let's try to figure out how a common man would manage such plans.

Rule1#: If you have to provide some guarantee, you will have to charge some money for that. That money has to be taken from the fund value.

Rule2#: Stock market can never be guaranteed anything. It may crash anyway. So fund managers will have a pressure to minimize their risk and keep money in debt instruments and fixed deposits.

Rule3#: Since the lock in period is pretty big, 7-10 years, some amount of market risk can be adjusted here and there.

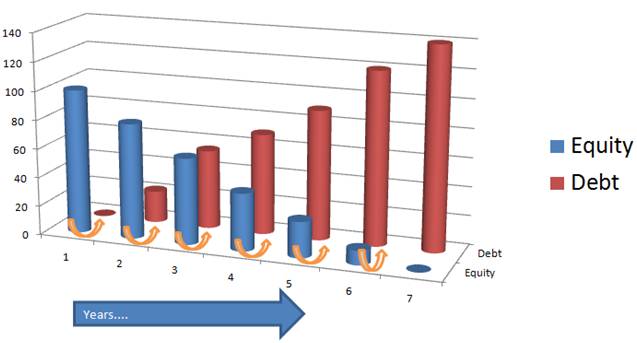

Let’s assume that the average interest on a secure debt instrument will be 7%. For the sake of simplicity I am assuming that the fund administration charges and other charges are 0.

Suppose the current NAV (and total fund value) is Rs 100. The fund manager wisely allocates the money in stock market, and after 1 year it gives 20% returns. The total NAV is Rs 120. Now the fund manager has the obligation to pay at least Rs 120 after 9 years. Now fund manager cannot take the risk of putting everything in stock market as it doesn't come with the guarantee. The debt product gives the guarantee. So the fund manager will have to pass a portion of total fund value to debt product to assure Rs. 120.

X*(1.07) ^9 = 120 gives X as ~ 65.

So the fund manager will allocate Rs 65 to some debt product and 120-65 to equity market again.

Let’s say after another year, the market resulted in good returns, and Rs 55 invested in the market sees another 20% jump. Now the total fund value becomes 65*1.07 + 55*1.2 ~ 146. Now the fund manager has the obligation to pay at least 146 Rs after 8 years. To provide this fund manager will need to solve this equation.

65*(1.07) ^9 + Y*(1.07)^8 = 146

This gives Y ~ 11.

Now fund manager will allocate additional Rs 11 to debt market, and put rest 44 in the equity market.

Let’s assume this process continues and after 6th year you have assured sum as Rs 180. By that time the equity component will be almost negligible and even if the market is highly volatile, it will not affect the fund value.

So absolute returns after 7 years will be 80%. (This is another gimmick, they will immediately say, sir which bank assures 80% returns and YES THEY DO SAY SO). If we calculate the effective rate of annual return it will come around ~8.7%. Which is marginally better than an FD (if we include the tax saving, it may be a bit better) but do we really want ~9% from the equity market for next 7 years period? Even the balanced mutual fund will give much more than 12% for this time frame. The few best MFs in my view have given more than 25% over the period of 15 years.

Pictorial representation of what I wrote will be like this.

Let’s have a close look at how a possible highest NAV plan will work. They use Dynamic Hedging and Constant Proportion Portfolio Insurance. Although I don't fully understand these concepts, we actually don't need to digest this financial alchemy. Let's try to figure out how a common man would manage such plans.

Rule1#: If you have to provide some guarantee, you will have to charge some money for that. That money has to be taken from the fund value.

Rule2#: Stock market can never be guaranteed anything. It may crash anyway. So fund managers will have a pressure to minimize their risk and keep money in debt instruments and fixed deposits.

Rule3#: Since the lock in period is pretty big, 7-10 years, some amount of market risk can be adjusted here and there.

Let’s assume that the average interest on a secure debt instrument will be 7%. For the sake of simplicity I am assuming that the fund administration charges and other charges are 0.

Suppose the current NAV (and total fund value) is Rs 100. The fund manager wisely allocates the money in stock market, and after 1 year it gives 20% returns. The total NAV is Rs 120. Now the fund manager has the obligation to pay at least Rs 120 after 9 years. Now fund manager cannot take the risk of putting everything in stock market as it doesn't come with the guarantee. The debt product gives the guarantee. So the fund manager will have to pass a portion of total fund value to debt product to assure Rs. 120.

X*(1.07) ^9 = 120 gives X as ~ 65.

So the fund manager will allocate Rs 65 to some debt product and 120-65 to equity market again.

Let’s say after another year, the market resulted in good returns, and Rs 55 invested in the market sees another 20% jump. Now the total fund value becomes 65*1.07 + 55*1.2 ~ 146. Now the fund manager has the obligation to pay at least 146 Rs after 8 years. To provide this fund manager will need to solve this equation.

65*(1.07) ^9 + Y*(1.07)^8 = 146

This gives Y ~ 11.

Now fund manager will allocate additional Rs 11 to debt market, and put rest 44 in the equity market.

Let’s assume this process continues and after 6th year you have assured sum as Rs 180. By that time the equity component will be almost negligible and even if the market is highly volatile, it will not affect the fund value.

So absolute returns after 7 years will be 80%. (This is another gimmick, they will immediately say, sir which bank assures 80% returns and YES THEY DO SAY SO). If we calculate the effective rate of annual return it will come around ~8.7%. Which is marginally better than an FD (if we include the tax saving, it may be a bit better) but do we really want ~9% from the equity market for next 7 years period? Even the balanced mutual fund will give much more than 12% for this time frame. The few best MFs in my view have given more than 25% over the period of 15 years.

Pictorial representation of what I wrote will be like this.

So what is my conclusion today?

Whenever someone is guaranteeing something, please ask...what is the cost of guarantee? Are you into charity? :-)

Whenever someone is guaranteeing something, please ask...what is the cost of guarantee? Are you into charity? :-)

No comments:

Post a Comment